In our latest Flows magazine, we focus on sustainability. Today, we take a closer look at the Corporate Sustainability Reporting Directive or CSRD for short.

CSRD provides for detailed reporting requirements that require companies to map the environmental and social impact of their activities as well as governance aspects, in addition to their financial situation. It also defines indicators on which companies must report.

For whom? The new directive applies to all large companies that meet at least two of the following criteria:

- A net turnover of €40 million;

- A balance sheet total of €20 million;

- An average of 250 employees during the financial year.

Double materiality

An important novelty is the concept of double materiality. This requires companies to report to what extent sustainability issues affect their business and to what extent their business activities have an impact on people and the environment. The concrete implementation of the double materiality principle is done according to two perspectives:

On the one hand, the outside-in perspective (financial materiality): this includes the risks and opportunities of ESG issues on the company’s financial health and operational performance. This involves identifying the magnitude and likelihood of the impact of an ESG theme.

For example, the war in Ukraine leading to production disruptions. Or a company located in flood-prone areas. In the case of an effective flood with damage, the financial impact will be found in the company’s financial statements.

On the other hand, the inside-out perspective (impact materiality): this refers to the size, scope and irreparable nature of the impact of an ESG issue on people and society. The size looks specifically at the impact on people and society, the scope refers to the geographical size of the impact and the irreparable nature deals with the reduction possibilities of the negative impact. Examples here are biodiversity loss or human rights violations potentially occurring in the construction sector; or a company’s emissions in a residential area.

To measure is to know

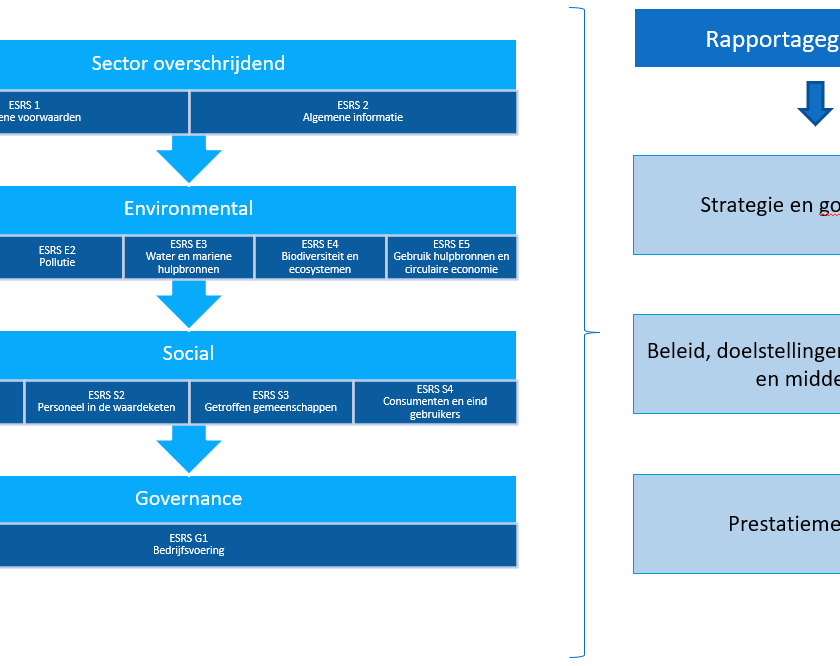

The data collection for the dual materiality analysis is aligned with the ‘European Sustainability Reporting Standards’ (‘ESRS’). The ESRS (see figure) consist of 12 standards: two general overarching standards and three thematic topics, of which five standards under the environmental component, four standards under the social component and one standard under the good governance component.

Companies are required to report on the general strategy, governance and assessment disclosure requirements (ESRS2). Further reporting obligation depends on the results of the double materiality.

Important: The methodology and data should be validated by the auditor.

CSRD-proofing in 5 steps

1. Determine risk landscape

2. Double materiality

3.

4. Strategy and actions

5. Due diligence and reporting